Buy Now, Pay Later (BNPL) services have become increasingly popular in recent years, offering consumers immediate purchases without the immediate financial burden. While these services can provide convenience and flexibility for many users, there are potential pitfalls that individuals should be mindful of when thinking about BNPL options. As teenagers navigate the allure of BNPL as they get older, it’s crucial for them to understand the potential risks involved and develop responsible financial habits early on to avoid falling into the traps of unchecked spending and mounting debt.

Related: Money management for teens

What is Buy Now, Pay Later (BNPL)?

Buy Now Pay Later has become an increasingly popular option when shopping online, thanks to platforms like Klarna, Clearpay and Laybuy.

These give shoppers the option to ‘try before they buy’ and pay 30 days later – or split the cost into three equal payments, often with the promise of no added fees, interest or late charges. You’ll spot these platforms at the checkout of dozens of big name retailers, but critics say that they tempt young people to spend more than they can afford.

Since these platforms enable customers to make use of a credit facility and are intended to be used only by those aged 18+, it’s important to note that we’re unable to allow the GoHenry card to be used with Klarna or Clearpay. If a transaction is attempted, it will be automatically declined – so please make your child aware of what it means to Buy Now, Pay Later (BNPL), and why they need to select the ‘card payment’ option at checkout, before using their GoHenry card online.

A small number of retailers now have their entire checkout process – including immediate card payments – managed by Klarna. Unfortunately, this means that even immediate card payments will be automatically declined when using a GoHenry card simply because they are processed via the Klarna platform.

How old do you need to be to use Buy Now, Pay Later?

In the UK, BNPL services require users to be at least 18 years old to use their services. This age restriction aligns with the legal age for entering into financial contracts and credit agreements.

Additionally, as young users become old enough, they should consider the potential financial implications before engaging in BNPL transactions to ensure responsible and informed financial decision-making.

Which retailers offer Buy Now Pay Later?

There are three main Buy Now Pay Later platforms available in the UK: Klarna, Clearpay and Laybuy. Of these, Klarna is the biggest and the best known, with over 90 million active consumers across more than 250,000 retailers in 17 countries. In the UK alone, Klarna has over seven million customers.

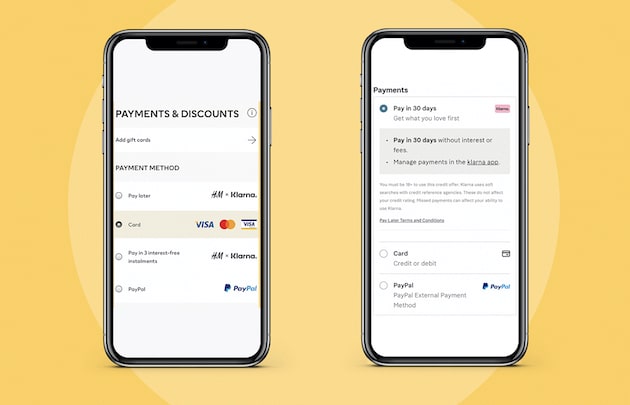

Buy Now Pay Later is offered as a payment option at the checkout by a large number of retailers – including many of the stores which we know are most popular with GoHenry customers, such as ASOS, H&M, New Look and JD Sports.

Some stores give customers a choice of payment options: card payments, Klarna’s Pay in 30 days / Pay in 3 instalments, or pay with external platforms such as Paypal or Apple Pay. Klarna also offers financing, which is available for bigger purchases over a longer time frame of up to 36 months.

Clearpay gives customers the ability to pay in instalments without paying any interest. Clearpay then automatically processes card payments on the scheduled dates.

How does Buy Now Pay Later work?

In most cases, when you checkout and choose the card payment option, your payment will be taken in the usual way. But if you choose to pay later, Klarna payments won’t be due until 30 days after you place your order. If you opt for ‘Pay in 3 instalments’ or financing, your first instalment will be taken immediately, and subsequent payments will be automatically taken from your card on a set date.

When you use Clearpay, the first payment will be taken immediately, with three more payments scheduled over the following six weeks.

Given the range of payment options offered at checkout, some younger customers might not understand the difference between them – and risk having their payment declined as a result. This is why it’s so important to ensure that they’ve selected the card payment option rather than Pay in 30 days or Pay Later / Afterpay.

It’s important to note that customers must be at least 18 to use the pay later options, and Klarna conducts a ‘soft’ credit check and affordability assessment before these can be approved.

Clearpay requires customers to verify their age and identity with a passport, driver's license, utility bill or bank statement.

As an added layer of protection for our young customers, we’ve blocked GoHenry cardholders' ability to pay using Klarna or Clearpay.

Does it cost anything to use Klarna or Clearpay?

In the UK, there are no interest or late payment fees associated with Klarna’s Pay in 30 days or Pay in 3 instalments, so it won’t cost any more than if you paid for the item upfront. If payments are late, this won’t affect your credit score, but if a payment is several months overdue, it may be passed to a debt collection agency. Interest is only payable if you use Klarna financing.

If you use Clearpay, there are no charges unless you make a late payment, in which case you’ll be charged £6. Late fees are capped at £36 for orders above £24 or £6 for orders under £24.

The pros and cons of Buy Now Pay Later

Pros

-

BNPL offers consumers immediate purchases without the immediate financial burden.

-

These services can provide convenience and flexibility for many users, especially at expensive times of the year, like Christmas.

-

BNPL services provide the option to spread the cost of a purchase over several instalments. This can make expensive items more affordable, allowing users to budget and manage their finances more effectively.

-

Many BNPL plans offer interest-free periods, meaning users can avoid paying additional charges if they repay the full amount within a specified timeframe. This can be advantageous for those who can manage their payments responsibly.

Cons

-

The ease of access to BNPL credit and deferred payment can create a scenario where impulsive spending habits may lead to financial stress.

-

BNPL can lead to debt accumulation, impacting the financial well-being of users.

-

If you fall behind on your BNPL plan payments, you'll be reported to the credit bureaus. Once that happens, your credit score could take a big hit.

-

While many BNPL services offer interest-free periods, failure to repay the full amount within the specified timeframe can result in high-interest rates and fees. Users may end up paying more than the original purchase price.

For the above reasons, we recommend talking to children about needs versus wants and starting a conversation with teenagers about credit and debt so that they’re fully informed about handling credit responsibly.

For more information about Buy Now Pay Later, please take a look at our FAQs.

How can GoHenry help?

GoHenry is a prepaid teen debit card that can help teens in several ways. Not only does it give teens the independence to use a debit card in the real world, but it also helps them learn about the value of money and how to make smart financial decisions. It teaches them about money management and the importance of tracking their spending, and also allows them to set savings goals.

Related articles:

Teaching your teenager the value of money

How to teach delayed gratification to kids

Common financial problems for teens